(FREE) The Basics of Cash Flow Statements, Part 1

(FREE) The Basics of Cash Flow Statements, Part 1

Cash flow statement. Operations. Working capital.

Commentary directly from the video (regular type)

My commentary (italics)

Intro

The cash flow statement tells you how effectively you manage your cash. It’s cash, of course, that you use to pay your vendors, employees, and taxes. When you can’t do that anymore - it’s game over. As long as there’s cash available to do those things, you can live to fight another day.

The cash flow statement

Profit does not equal cash. At least it doesn’t if you’re using accrual accounting. Ask your bookkeeper if you’re not sure whether your books are accrual basis OR cash basis.

Most of what follows will only apply if you’re using accrual accounting.

Revenue earned does NOT mean you received cash. Expenses incurred do NOT mean you spent cash. Eventually, you will receive this cash and spend this cash. But, it often does not happen immediately. As you’ll see later - the effect of accounts receivable/payable, inventory, and other factors will tell you why your net income is not the same as your cash from operations.

Yes, if you want to know how much cash your business has at any given time - you could just look at your balance sheet. However, this WON’T tell you how the cash came into the business and what it was spent on. The cash flow statement will.

Remember, from last week’s post “The cash flow statement is a CRUCIAL link between your profit & loss statement and your balance sheet.”

Components of the cash flow statement

Operations

This is the most important section

How much cash was received from selling your products and/or services

How much cash was spent on inventory, employees, overhead, etc?

Cash that is received and spent in the normal course of the company’s business

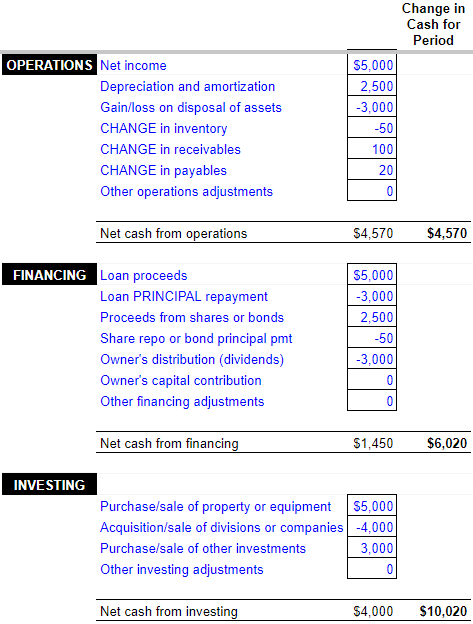

Investments

Outside of your primary business activities

How much cash was spent on machinery or equipment

How much cash was received from the sale of investments

Cash that was converted to other assets

Financing

Also outside of your primary business activities

How much cash was received from borrowing or raising capital

How much cash was spent repaying borrowed money or paying dividends

Cash that was transferred into or out of the business

The sum of these three sections = your net change in cash for the period. This will also = the difference in your beginning and ending cash balance (from the balance sheet).

BEGINNING CASH

+ CASH FROM OPERATIONS

+ CASH FROM (USED IN) INVESTING

+ CASH FROM (USED IN) FINANCING

= ENDING CASH

Keep in mind that cash flow from investments will often be negative. Hopefully, cash flow from operations is usually positive!

Cash flow from operations - in detail

There are two methods to calculate cash flow from operations. Both achieve the same result.

Indirect method

Starts with net income and makes adjustments related to accounts payable/receivable, inventory, and other factors

Not as intuitive as the direct method

Use the free The Basics of Cash Flow Statements, Part 1 spreadsheet to better understand the indirect method

Much easier to prepare

Direct method

Lists different types of transactions that affect cash

For example, cash received from customers, cash paid to suppliers, cash paid to employees, taxes, interest paid, and so on…

Very time-consuming to prepare

The indirect method will be referenced in the video and in this section.

To determine your cash flow from operations via the indirect method - the following calculation must be made:

CASH FROM OPERATIONS =

Net income (loss)

+ Depreciation & amortization

+/- Gain/loss on disposal of assets

+/- Change in inventory

+/- Change in receivables

+/- Change in payables

+/- Any other operational adjustments

For a more in-depth explanation of each factor that affects cash flow - see the free The Basics of Cash Flow Statements, Part 1 spreadsheet.

Depreciation and amortization

This is listed as an expense in the income statement. However, depreciating an asset has no effect on cash. It is just an accounting entry.

Cash was affected when you bought the asset - something we’ll cover in the investing section. Remember, we’re adjusting net income to reflect your cash flow from operations. So, depreciation and amortization get added back to it.

Effect on cash: Increase.

Gain/loss on disposal of assets

This is also listed as an expense on the income statement. But, like depreciation and amortization, this accounting entry has no effect on cash. Cash is only affected by the sale price and purchase cost of assets. NOT whether you sold those assets for more or less than their depreciated value.

Again, the sale and purchase of assets will be addressed in the investing section. So, we will reverse what happened on the income statement.

Effect on cash: Increase (loss) or decrease (gain).

CHANGE in inventory

This is NOT your inventory balance at the end of the period. It is the amount (increase or decrease) your inventory changed over the period.

For instance, say your inventory balance at the beginning of the period was $100 and at the end of the period it was $150. That’s a $50 increase. You paid for this increase in inventory with cash, of course.

You know that net income includes the cost of goods sold (cost of sales). But it DOESN’T capture if you are buying more inventory than you are selling. Or selling more than you are buying.

Effect on cash: Increase (selling more than buying) or decrease (buying more than selling).

CHANGE in receivables

Again, this is NOT your receivables balance at the end of the period. It is the amount (increase or decrease) your receivables changed over the period.

Receivables are sales (included in net income) that are on credit. This means that cash has NOT been received. So, it needs to be reversed out of net income.

If your receivables increased - you sold more on credit. This is fine and good for revenue and net income, but it has not (as of yet) increased cash!

Effect on cash: Increase (selling less on credit) or decrease (selling more on credit)

CHANGE in payables

One more time… this is NOT your payables balance at the end of the period. It is the amount (increase or decrease) your payables changed over the period

Payables work in the opposite manner as receivables. Payables are expenses (included in net income) that are on credit. This means that cash has NOT been paid. So, it needs to be reversed out of net income.

If your payables increased - you bought more on credit. This has affected net income, but it has not (as of yet) affected cash.

Effect on cash: Increase (buying more on credit) or decrease (buying less on credit).

Hopefully, you can see how vital managing working capital (inventory, receivables, and payables) is to the cash flow of your business!

Read more in Part 2:

Comment below

Is managing your working capital (receivables, payables, and inventory) a priority?

If so, what tactics do you use to manage this critical aspect of cash flow?